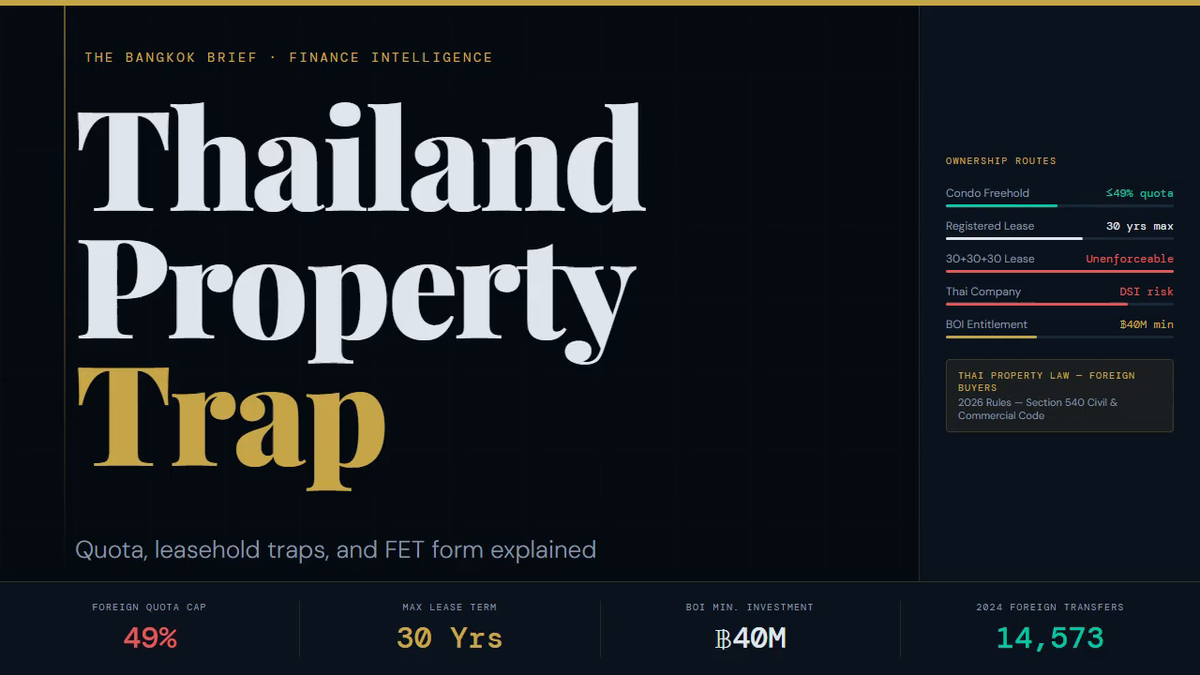

Thailand Property for Foreigners: Condo Quota & Lease Traps

In Thailand, a foreigner can legally own a condo freehold — but only if the building's foreign quota has not been exhausted, only if the purchase funds arrived from overseas in foreign currency with a documented paper trail, and only if the title registration is completed at the Land Department before any ownership dispute arises. Miss any one of those three conditions and your ฿6,200,000 does not buy you a title deed. It buys you a contract dispute with a developer who is under no legal obligation to return your deposit. This is the foundational reality every foreign buyer in Thailand must understand before signing anything.

The Four Foreign Ownership Routes in Thailand (2026)

There are four legal pathways for a foreigner to hold Thai property in 2026. Each carries different rights, different risks, and different legal ceilings. Understanding which route applies to your situation — before you engage an agent — is the most important decision in the entire process.

1. Condo Freehold (Condominium Act)

This is the only route by which a foreigner can own Thai real estate outright in their own name. Under the Condominium Act, foreigners may collectively hold a maximum of 49% of the total floor area in any registered condominium building. Note carefully: this is floor area, not unit count. A single large-format foreign-owned penthouse can consume a disproportionate share of the quota. The remaining 51% must be held by Thai nationals or Thai juristic persons at all times.

Freehold condo ownership gives you a chanote title deed (nor sor 4 jor) — the strongest form of Thai land title — in your own name. You can sell, mortgage (to some lenders), and inherit the property. This is the route with the most genuine legal protection for foreign buyers.

2. Long-Term Lease (30-Year Registered Lease)

For landed property — houses, villas, townhouses — foreigners cannot own the land. The most common alternative offered by developers is a long-term lease. The legal reality here diverges sharply from the marketing language.

Section 540 of the Thai Civil and Commercial Code sets the maximum registrable lease term at 30 years. Any clause in a contract promising a "30+30+30" structure — giving a theoretical 90-year tenure — is legally unenforceable beyond the first registered 30 years. Renewal is at the discretion of whoever owns the land at renewal time. If the developer sells the land or dies, renewal clauses in a private contract are void against the new owner unless they were registered at the Land Department.

A lease not registered at the Land Department is void against any third-party buyer. Always verify that your lease is formally registered, not just documented in a private agreement.

3. Thai Company Ownership

Some advisors historically suggested that a foreigner could use a Thai-majority company — with compliant Thai shareholders holding 51% — to purchase land. In 2026, this route carries serious legal risk. The Department of Special Investigation (DSI) is actively investigating nominee shareholder structures. If the Thai shareholders are found to be nominees (holding shares on behalf of the foreigner without genuine economic interest), the structure is illegal under the Foreign Business Act. Penalties include land seizure. This is not a grey area — it is an enforcement priority.

4. BOI Investment Pathway

The Board of Investment offers a foreign land ownership pathway for qualifying investors. The minimum investment threshold is ฿40,000,000 into BOI-approved instruments (Thai government bonds, property funds, or direct equity in a promoted business). This entitles the investor to own up to 1 rai (1,600 sqm) of land for residential use. This route is relevant to a small subset of high-net-worth expats and is not a practical pathway for typical condo or villa buyers.

The 49% Quota: How It Actually Works

The quota is calculated at the building level, not the developer level or the project level. Each registered condominium juristic person has its own quota calculation. A developer building two towers on one site may have two separate quotas — or one combined quota, depending on how the juristic person is structured. Always check the specific building's Land Department registration.

The check must be done at the Land Department office with jurisdiction over the building's district. An agent's verbal assurance, a developer's sales office confirmation, or a lawyer's estimate based on old data is not sufficient. Quota status can change between the day you check and the day you sign if another foreign buyer registers in the intervening period. Best practice is to check quota status, sign, and move to registration as quickly as possible.

| Ownership Route | Property Type | Max Foreign Interest | Registered at Land Dept? | 2026 Risk Level |

|---|---|---|---|---|

| Condo Freehold | Condominium unit | 49% of building floor area | Yes — chanote in own name | Low (if quota verified) |

| 30-Year Lease | House, villa, land | 30 years (registered); renewal unenforceable | Yes — must be registered | Medium (renewal risk) |

| Thai Company | Any | 49% shareholding legally | Yes — in company name | High (DSI enforcement) |

| BOI Investment | Residential land (max 1 rai) | Full ownership | Yes — in own name | Low (if fully compliant) |

The FET Form: The Document Nobody Warns You About

The Foreign Exchange Transaction (FET) Form — sometimes called a Thor Tor 3 — is issued by a Thai bank when it receives an inbound international wire transfer in foreign currency. It is proof that your purchase funds originated overseas and were converted to Thai baht on arrival in Thailand.

Without a valid FET form covering the full purchase price, the Land Department will not register a foreign condo title. This is a hard rule with no exceptions and no workarounds.

The practical implications are significant:

- Do not fund your Thai condo purchase from a local Thai bank account, even if that account holds funds you originally brought from overseas. The paper trail is broken.

- Wire the full purchase amount directly from your overseas bank account to your Thai bank account in the same foreign currency (USD, GBP, EUR, AUD, etc.). Do not convert before sending.

- Ensure the receiving Thai bank issues a FET form for each inbound wire. For large purchases, you may need multiple wires — each must have its own FET form, and the sum must equal or exceed the purchase price stated on the contract.

- Keep FET forms permanently. They are also required if you later sell the property and wish to repatriate the proceeds.

Worked Example: Buying a ฿6,200,000 Bangkok Condo as a Foreign Buyer

Let's walk through what a compliant purchase looks like, and where the process breaks down.

Scenario: A British national (non-resident for UK tax purposes, holding a Thai DTV visa) purchases a freehold condo in a Bangkok mid-rise for ฿6,200,000. He is purchasing from a developer, not a resale.

Step 1: Quota Verification

Before signing, he visits the Land Department office for the district (e.g., Huai Khwang district office for a Ratchada property). He requests the current foreign ownership percentage for the specific juristic person ID of the building. The officer confirms: 41.3% of floor area is currently foreign-held. The quota is open. He proceeds.

Step 2: FET Form — The Wire

The purchase price is ฿6,200,000. At a rate of approximately ฿43.5 to the pound (2026 indicative rate), he needs to wire approximately £142,530 GBP from his Barclays account to his Bangkok Bank account in Thailand. He wires £145,000 to allow for transfer fees and rate movement. Bangkok Bank receives the GBP wire and converts it to ฿6,307,500. Bangkok Bank issues a FET form for ฿6,307,500 — more than the purchase price. This is acceptable; the FET form must cover at least the full purchase price.

Step 3: Transfer Tax and Fees

At the Land Department, the following costs apply on a new developer sale:

- Transfer fee: 2% of the appraised value (government assessed value, typically lower than market price). On a ฿5,800,000 appraised value: ฿116,000. Often split 50/50 between buyer and seller — negotiate this in the contract.

- Specific Business Tax (SBT): 3.3% of appraised or sale price (whichever is higher) if the developer has held the unit for fewer than 5 years — applicable on virtually all new developer sales. On ฿6,200,000: ฿204,600. Typically paid by developer on first-sale units — confirm in contract.

- Stamp duty: 0.5% — only applicable if SBT is not. On new developer sales, SBT applies, so stamp duty is waived.

- Withholding tax: Paid by seller (developer). Not a buyer cost on new purchases.

Total buyer-side closing cost estimate (buyer's share of transfer fee only): ฿58,000. Total with legal fees (฿15,000–฿30,000 for a competent property lawyer): ฿73,000–฿88,000.

Step 4: Title Registration

The buyer presents his passport, the signed purchase contract, the FET form, and the developer's documents at the Land Department. The officer verifies quota status again on the day of transfer. Title is registered. A chanote deed in his name is issued. He is the legal owner.

What Happens When It Goes Wrong

The scenario in the video introduction is not rare. A buyer signs a purchase contract. The quota was open at signing. Three months later — between contract signing and Land Department registration — another foreign buyer in the same building registers a large-format unit. The quota tips past 49%. At the registration counter, the Land Department rejects the transfer.

At this point, the buyer's options are:

- Negotiate with the developer to switch to a different unit in the Thai quota (51% zone) — these units are often lower floor, different aspect, or priced differently

- Negotiate a full deposit refund — the developer is not automatically obligated to refund; this depends on contract terms

- Pursue civil litigation — slow, expensive, and outcomes are uncertain

The protection is simple: include a quota-contingency clause in the purchase contract that makes the contract void (with full deposit refund) if the foreign quota is unavailable at the time of Land Department registration.

The Pre-Signing Checklist

- Quota check: Verify remaining foreign floor area percentage at the Land Department — not with the agent, not with the developer

- Title type: Confirm the unit has a chanote title deed (nor sor 4 jor), not a nor sor 3 gor or lower title

- FET form plan: Confirm your bank can issue FET forms for international wires and that you will wire from an overseas account in foreign currency

- Lease registration (if leasehold): Confirm the lease is or will be registered at the Land Department — not just recorded in a private contract

- Company structure check: If a Thai company is involved anywhere in the ownership chain, get independent legal advice on nominee risk before proceeding

- Quota-contingency clause: Insist this is written into the purchase contract before you pay any deposit

Frequently Asked Questions

Can I buy a Thai condo and put it in my spouse's name if they're Thai?

Yes, but with an important caveat. If you are married to a Thai national and wish to register the property solely in their name, the Land Department will require you to sign a declaration confirming that the funds used for purchase are your spouse's personal property, not marital assets. This prevents you from later claiming ownership rights. If you are unwilling to sign this declaration, the purchase may be delayed or rejected. Seek legal advice on marital property rules under Thai law before proceeding.

Is a 30-year lease actually safe for a retirement home?

It depends entirely on what you need the property for and your time horizon. A properly registered 30-year lease gives you genuine legal protection for those 30 years — you cannot be evicted by a new owner if the land is sold, provided the lease is registered. The risk is what happens at year 30. If the landowner (or their heirs) refuses renewal, or increases the renewal price dramatically, you have no legal recourse. For a 10–15 year retirement stay, a registered lease may be perfectly adequate. For an asset you intend to hold for 30+ years or pass to heirs, it is structurally unsuited.

Can I get a mortgage in Thailand as a foreigner?

Thai domestic banks do not typically offer mortgage lending to foreign nationals for property purchases. A small number of banks — notably Bangkok Bank and UOB Thailand — have offered limited mortgage products to foreigners with strong income documentation, long-term visas, and work permits, but these are not standard products and terms are restrictive. Most foreign buyers purchase cash or arrange financing in their home country against other assets.

What happens to my condo if I die — can my family inherit it?

A foreign-owned condo can be inherited by foreign heirs under Thai law, but the heir must either be a foreigner who qualifies under the same foreign ownership rules (and the quota must still be available at the time of inheritance transfer) or a Thai national. If the quota in the building has since hit 49%, the heir may not be able to register the title in their name and may be required to sell the unit within a legally specified period (typically one year). This is a significant estate planning consideration that is almost never discussed at the point of purchase.

Does the FET form requirement apply to resale purchases as well as new developer sales?

Yes. The FET form requirement applies to any foreign national registering condo ownership at the Land Department, regardless of whether the purchase is from a developer or a private resale seller. The funds must have originated overseas in foreign currency. There are no exemptions for resale purchases, for buyers who have been resident in Thailand for many years, or for buyers who hold long-term visas. The rule is absolute at the point of Land Department registration.

Action Steps Before You Buy

- Identify the specific building juristic person ID and visit the relevant Land Department district office to verify the current foreign quota percentage — do this yourself, do not delegate it to an agent

- Engage an independent property lawyer (not the developer's recommended lawyer) before paying any deposit; budget ฿15,000–฿30,000 for a thorough contract review

- Instruct your overseas bank to wire the full purchase amount in your home currency to your Thai bank account; confirm with your Thai bank that they will issue a FET form upon receipt

- Ensure your purchase contract includes a quota-contingency clause providing for full deposit refund if foreign quota is unavailable at registration

- If considering a leasehold property, obtain written confirmation from the Land Department that the lease is or will be registered — and request a copy of the registered lease document, not just the private contract

- If any Thai company structure is involved, obtain an independent legal opinion specifically addressing nominee shareholder risk under the 2026 DSI enforcement environment before committing funds