Thailand Health Insurance: BUPA, AXA, Cigna & Pacific Cross Compared

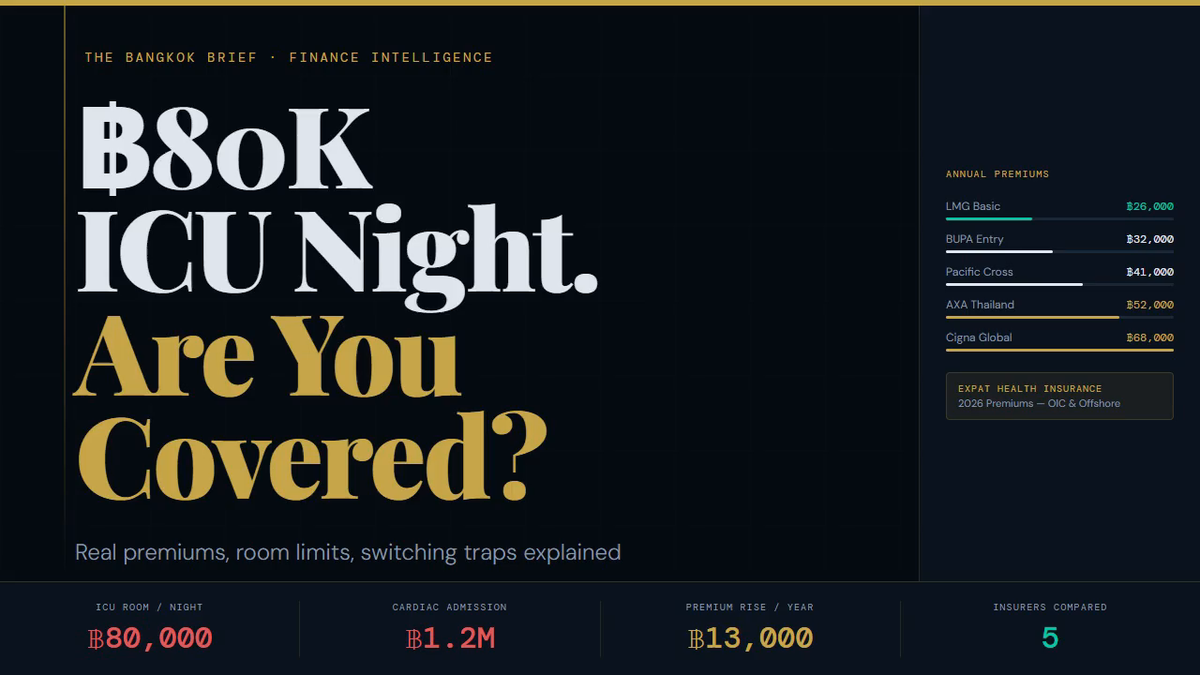

If you are living in Thailand without health insurance — or with a plan you have not read carefully — a single cardiac event can produce a bill between ฿400,000 and ฿1,200,000. That is not a worst-case estimate. That is the standard billing range for a five-day cardiac admission with intervention at a Bangkok private hospital in 2026. The room charge alone at Bumrungrad International runs ฿25,000 to ฿80,000 per night in the ICU. The question is not whether you need cover. The question is which plan actually covers what happens to you — and whether you will still be able to get it in five years.

Why Thai Private Hospital Costs Are Rising Faster Than Your Premium Expectation

Thai private hospital billing has inflated at 12–18% over the past two years. This is not driven by a single factor. It reflects rising specialist fee schedules, upgraded facilities competing for medical tourism revenue, and the same post-pandemic cost pressures affecting healthcare globally — compounded by a domestic market where Bumrungrad, Bangkok Hospital Group, and Samitivej set the pricing benchmark every other private hospital follows upward.

For expats, the direct consequence is visible in renewal letters. A BUPA Thailand IPD entry-level premium for a 35-year-old non-smoking male was approximately ฿18,000 in 2022. By 2023 it had risen to roughly ฿21,000, and by 2024–2025 it was tracking toward ฿27,000 or above for the same coverage tier. Across the market, average annual premium increases at renewal for ages 35–50 are running at ฿8,000–฿13,000 per year. That trajectory does not flatten as you age — it accelerates, because age-band reclassifications layer on top of medical inflation.

Thailand's Two-Tier Healthcare System: What Expats Are Actually Choosing Between

Thailand operates a genuine two-tier system. Public hospitals — from district hospitals to university hospitals like Siriraj — provide care that is free or nearly free for Thai nationals, technically accessible to foreigners, but characterised by long waits, Thai-language administration, and ward-based accommodation. For a routine illness these hospitals are functional. For a complex admission requiring specialist coordination, imaging, and English-language communication, they are not the realistic choice for most expats.

The private tier — Bangkok Hospital Group, Bumrungrad, Samitivej, Vejthani, BNH, Paolo, and their regional affiliates — delivers care that is genuinely world-class by international standards. JCI-accredited, English-speaking staff, same-day specialist access, and facilities that attract medical tourists from across Asia. But world-class care comes at world-class prices, and those prices are set without reference to what any insurer will or will not pay.

The Five Insurers Compared: BUPA, AXA, LMG, Cigna, Pacific Cross

The table below shows indicative 2025–2026 annual premiums for a 35-year-old male non-smoker seeking combined IPD and OPD cover. These figures reflect base-tier plans within each insurer's range — mid-tier and premium plans carry higher limits and higher costs. Always verify current rates directly with the insurer or a licensed broker, as premiums adjust at each policy anniversary.

| Insurer | Plan Tier | Annual Premium (approx.) | IPD Annual Limit | OPD Included | Jurisdiction |

|---|---|---|---|---|---|

| BUPA Thailand | IPD Entry + OPD | ฿27,000–฿34,000 | ฿1,500,000–฿3,000,000 | Yes (limited) | Thai OIC |

| AXA Thailand | SmartCare / FlexiCare | ฿25,000–฿40,000 | ฿1,000,000–฿5,000,000 | Yes (add-on) | Thai OIC |

| LMG Insurance | Super Care Basic/Plus | ฿22,000–฿38,000 | ฿1,000,000–฿4,000,000 | Yes (tiered) | Thai OIC |

| Cigna Thailand | HealthFirst / GoHealth | ฿28,000–฿45,000 | ฿2,000,000–฿10,000,000 | Yes | Thai OIC / Regional |

| Pacific Cross | Essential (Thailand-only) | ฿26,000–฿32,000 | ฿3,000,000–฿6,000,000 | Yes | Regional (non-OIC) |

| Pacific Cross | Essential (Regional) | ฿38,000–฿52,000 | ฿3,000,000–฿6,000,000 | Yes | Regional (non-OIC) |

The Room Sub-Limit Trap: The Most Expensive Mistake Expats Make

Many entry-level Thai health insurance plans impose a room and board sub-limit — a per-night cap on what the insurer will pay for your hospital room. The most common sub-limits in the market sit at ฿3,000 to ฿4,500 per night.

This sounds adequate until you check the room rate at the hospital you will actually go to. A standard private room at Bumrungrad starts at approximately ฿6,500 per night. A semi-private room at Bangkok Hospital runs ฿4,800–฿7,000. An ICU bed at either hospital is ฿25,000–฿80,000.

The arithmetic is brutal: a plan with a ฿4,500/night room sub-limit at a hospital charging ฿6,500/night leaves you paying ฿2,000 per night out of pocket, every night, on top of your premium. For a ten-day admission that is ฿20,000 in uncovered room costs alone — before a single drug, test, or specialist fee. For an ICU admission it is catastrophic.

The fix is simple but must be done before you are admitted: check whether your plan has a room sub-limit, and if so, whether it matches the actual room rate at your preferred hospital. If it does not, either upgrade to a plan without a sub-limit or select a hospital whose rates fall within your covered band.

Insurer Jurisdiction: Why This Is Not a Footnote

BUPA Thailand, AXA Thailand, and LMG are regulated by Thailand's Office of Insurance Commission (OIC). When a claim is disputed, the OIC is the regulatory backstop — complaints go through Thai administrative channels and, ultimately, Thai courts. Policies are governed by Thai law and issued in Thai.

Pacific Cross regional plans and certain Cigna international plans operate under different jurisdictions — typically Hong Kong or Singapore law for regional policies, with claims processes that run outside the Thai OIC framework. This is not inherently better or worse. It is different in practice, particularly if you need to escalate a denied claim. An OIC-regulated insurer faces regulatory consequences in Thailand for bad-faith denials. A non-OIC plan requires you to pursue disputes through a foreign legal framework.

For most expats on straightforward plans, jurisdiction never becomes relevant. For complex, high-value claims — exactly the ones that matter — it becomes the only thing that matters.

The Switching Trap: Why This Decision Is Semi-Permanent

Switching health insurers in Thailand is not like switching a phone plan or a bank account. It carries a risk that is permanent and irreversible: pre-existing condition exclusions on the new policy.

Consider a 47-year-old expat who had a back issue treated two years ago — a single GP visit, a course of physiotherapy, nothing surgical. When they apply to a new insurer, that insurer's underwriting team reviews their medical history. The back condition is now a named permanent exclusion on the new policy. Not a waiting period. Not a temporary exclusion. Excluded for the lifetime of the policy.

Meanwhile, their old insurer — if they had held that policy since before the back issue appeared — would have covered it under the continuity of cover provisions. By switching, they have permanently traded away coverage for a condition they already have.

The practical implications:

- If you are healthy and new to Thailand, lock in coverage immediately — your underwriting history is clean and your options are widest.

- If you have held a policy for several years and developed any conditions, the cost of switching is not just the new premium — it is the permanent loss of coverage for everything that has happened to you since you took out the old policy.

- Before switching for any reason, request a pre-switch underwriting assessment from the new insurer in writing. Do not cancel the old policy until the new policy is issued and you have reviewed the exclusions schedule.

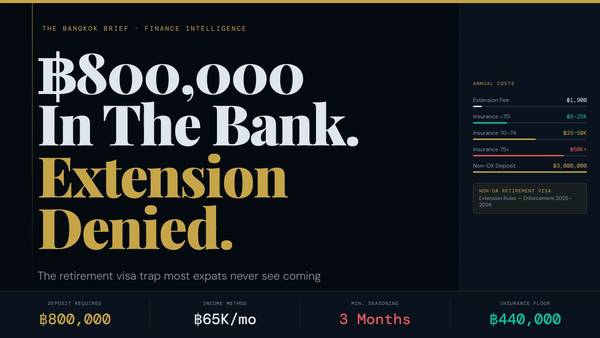

Visa Requirements: What the Non-OA Needs

Expats applying for or renewing a Non-Immigrant OA (retirement) visa must demonstrate health insurance coverage meeting the following minimums set by the Thai government:

- Outpatient (OPD): minimum ฿40,000 annual coverage

- Inpatient (IPD): minimum ฿10,000 per illness/injury

Note that these minimums are extremely low relative to actual hospital costs. A compliant visa insurance policy is not the same as adequate health insurance. Many expats hold a visa-minimum plan as their only cover, which leaves them catastrophically exposed. The visa requirement is a floor, not a recommendation.

Digital Nomad visa (LTR Visa — Wealthy Pensioner / Remote Worker categories) carries its own insurance documentation requirements. Check the Board of Investment's current guidelines, as these are updated periodically.

Worked Example: What a Real Cardiac Admission Costs You Under Three Different Plans

Scenario: 55-year-old British expat, male, admitted to Bumrungrad for five days following a cardiac event requiring stenting. Total hospital bill: ฿850,000.

Plan A: Budget plan, ฿3,500/night room sub-limit, ฿1,000,000 IPD limit

- Room charge: 5 nights × ฿8,500 (standard private room) = ฿42,500 billed. Insurer pays 5 × ฿3,500 = ฿17,500. You pay: ฿25,000 in room shortfall.

- Procedure, specialist, anaesthesia, drugs, imaging: ฿807,500 — within the ฿1,000,000 IPD limit, so covered (subject to any co-pay or deductible).

- Total out of pocket: approximately ฿25,000–฿60,000 depending on co-pay structure and any uncovered items.

Plan B: Mid-tier plan, no room sub-limit, ฿3,000,000 IPD limit, ฿50,000 co-pay

- Room charge: fully covered.

- All other charges: covered above co-pay.

- Total out of pocket: ฿50,000 co-pay only.

Plan C: Self-insured (no cover)

- Total out of pocket: ฿850,000.

- At 55, future insurability for cardiac conditions: zero. Permanent exclusion on any future policy.

The premium difference between Plan A and Plan B for a 55-year-old is likely ฿15,000–฿25,000 per year. One cardiac admission eliminates that "saving" twenty times over.

Frequently Asked Questions

Can I get health insurance in Thailand if I already have a pre-existing condition?

Yes, but with exclusions. Thai OIC-regulated insurers and most regional insurers will issue a policy with named exclusions for disclosed pre-existing conditions. You will receive coverage for everything else. The critical rule: always disclose fully and accurately. Failure to disclose and then making a claim on that condition is grounds for policy cancellation and fraud allegations — not just a denied claim.

Is OPD cover worth the additional premium?

For most expats under 50 in reasonable health, OPD cover adds ฿5,000–฿15,000 per year to a premium. If you visit a GP or specialist more than three or four times a year, it pays for itself. If you are generally healthy and rarely seek outpatient care, IPD-only cover with a separate small fund for OPD costs is often more efficient. The key trap: do not buy OPD cover from a hospital-specific plan that only pays at one hospital group.

What happens to my Thai health insurance if I leave Thailand for more than 6 months?

It depends entirely on your policy terms. OIC-regulated Thai policies typically cover treatment in Thailand and may have limited or zero overseas cover. If you leave Thailand for an extended period, review your policy's geographical scope clause. Some plans lapse or become void if you are no longer resident. Regional plans from Pacific Cross or international Cigna products handle this differently — coverage follows you. This is a key reason some long-term expats with travel flexibility choose regional cover despite the higher premium.

My employer provides group health insurance. Do I need a personal policy too?

Group cover in Thailand is typically tied to employment. The day your employment ends, the cover ends — and if you have developed any conditions during the group cover period, they will be excluded on any individual policy you subsequently apply for. The strategic move is to hold a personal individual policy alongside employer cover from the day you arrive, while you are still healthy and insurable at standard rates. Continuity of the individual policy protects you when the group cover disappears.

How does Thai health insurance interact with the new income tax rules for long-stay expats?

Under the Revenue Department's updated guidance effective from 2024, foreign-sourced income remitted to Thailand by Thai tax residents is potentially assessable. Health insurance premiums paid to Thai OIC-regulated insurers may qualify for a tax deduction of up to ฿25,000 per year under existing personal deduction rules — but this applies to Thai-issued life and health policies, not to offshore international health plans. If you are a Thai tax resident and paying for a Thai OIC policy, confirm with a licensed Thai tax adviser whether your premium qualifies for the deduction. It is not automatic.

Action Steps

- Pull out your current policy tonight and locate three numbers: your room and board sub-limit per night, your annual IPD maximum, and your co-pay or deductible. Compare the room sub-limit to the actual room rate at your preferred hospital.

- If you are new to Thailand, apply for individual health insurance within your first 30 days — before any GP visits, prescriptions, or medical consultations create an underwriting history that follows you.

- Before switching any plan, request a written pre-underwriting assessment from the new insurer listing all conditions that will be excluded. Do not cancel the old policy until the new policy is in hand and you have compared exclusion schedules.

- Check your room sub-limit against the actual room rate at Bumrungrad, Bangkok Hospital, or whichever private hospital you would realistically use. If there is a gap of more than ฿1,500 per night, price an upgrade or a plan without a sub-limit.

- If you hold employer group cover, price an individual policy now while you are healthy. The cost of waiting is paid in permanent exclusions — not in premiums.