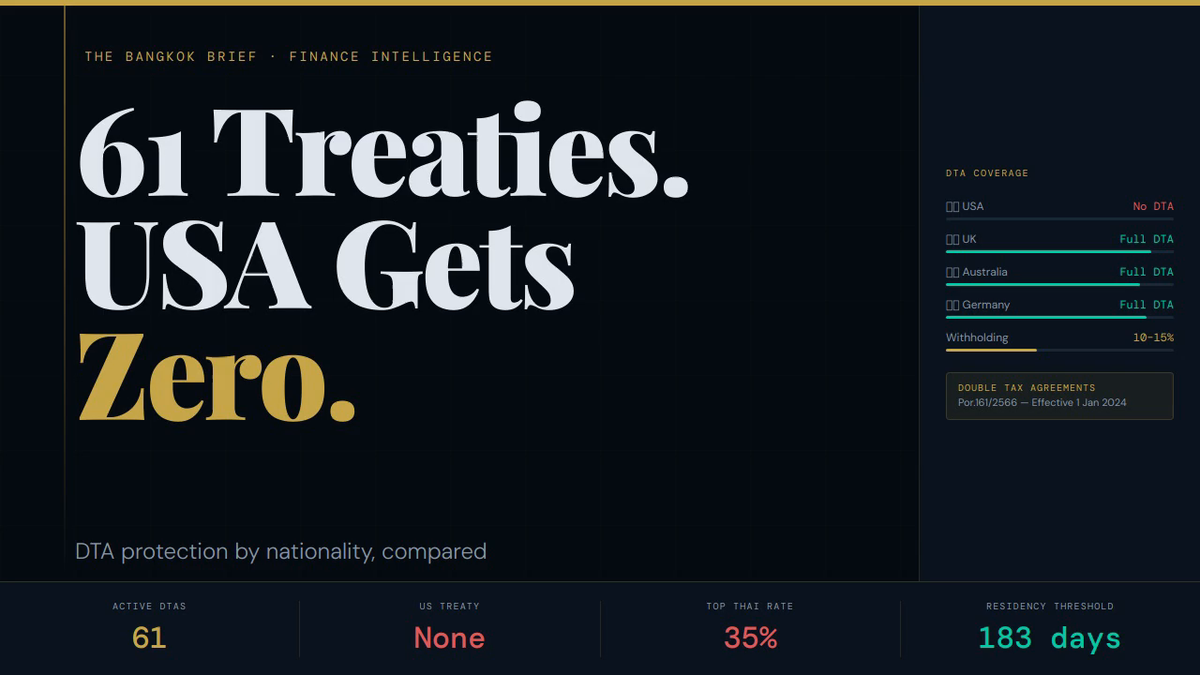

Thailand Double Tax Treaties: UK, US, Australia & Germany

If you are a tax resident in Thailand in 2026 — meaning you spend 183 or more days in the country — the passport you hold is now one of the most important financial variables in your life. The United States has no Double Tax Agreement with Thailand. The UK, Australia, and Germany do. That single fact can mean the difference between paying 0% and 35% on the same income, remitted from the same foreign account, by two neighbours living on the same Bangkok soi. This article explains exactly how Thailand's DTA network works, what each major treaty covers, and what the 2024 rule change under Por 161/2566 means for every expat remitting money into Thailand.

What Is a Double Tax Agreement and Why Does It Matter in Thailand?

A Double Tax Agreement (DTA) — also called a tax treaty — is a bilateral agreement between two countries that determines which country has the right to tax specific categories of income when a taxpayer has connections to both. Without a DTA, you can be taxed twice on the same money: once in the country where it was earned, and again in the country where you are tax resident.

Thailand has 61 active DTAs. These treaties do not eliminate Thai tax entirely — they allocate taxing rights by income type. For some categories (government pensions, certain interest income), the treaty gives exclusive taxing rights to one country. For others (private pensions, dividends, rental income), it may give Thailand the right to tax but cap the rate below the standard Thai PIT rate. The treaty text — specifically, which articles apply to which income type — determines everything.

The 2024 Rule Change: Por 161/2566 and Why It Changed Everything

Before 1 January 2024, a long-standing Revenue Department interpretation allowed expats to remit foreign income earned in a prior tax year without Thai tax liability. That loophole is gone. Under Por 161/2566, effective 1 January 2024, all foreign-sourced income remitted to Thailand is assessable income for Thai tax purposes — regardless of when it was earned. If you are a Thai tax resident (183+ days in Thailand in a calendar year), and you transfer money from an overseas account into Thailand, that remittance is now potentially taxable.

This makes DTA analysis urgent, not academic. The treaty you hold — or don't hold — now directly determines your annual Thai tax bill on remitted income.

Thai Personal Income Tax Brackets (2026)

| Assessable Income (฿) | Tax Rate |

|---|---|

| 0 – 150,000 | 0% |

| 150,001 – 300,000 | 5% |

| 300,001 – 500,000 | 10% |

| 500,001 – 750,000 | 15% |

| 750,001 – 1,000,000 | 20% |

| 1,000,001 – 2,000,000 | 25% |

| 2,000,001 – 5,000,000 | 30% |

| Above 5,000,000 | 35% |

Filing deadline: 31 March of the following year (e.g., TY2024 returns were due 31 March 2025). The Thai Revenue Department has publicly signalled active enforcement for TY2024 onwards. Ignorance is no longer a viable strategy.

The United States: No DTA, No Protection

The US–Thailand tax treaty negotiation has stalled for decades. As of 2026, no DTA exists between the United States and Thailand. This is not a loophole or an oversight — it is simply the current legal reality.

What this means in practice: an American who is a Thai tax resident remitting foreign income has no treaty-based protection. Every baht of assessable remitted income is subject to standard Thai PIT rates — up to 35%. There is no mechanism within Thai domestic law to offset US taxes already paid against a Thai liability without a treaty credit provision. Americans must rely on the US Foreign Tax Credit (FTC) to avoid double taxation at the US end, but Thailand will still assess and collect at full PIT rates on its side.

Americans should also note that the US taxes its citizens on worldwide income regardless of residency — meaning an American in Bangkok may be filing and paying in both countries simultaneously, without a treaty to coordinate the two systems.

The United Kingdom: Strong Treaty, but Income-Type Dependent

The UK–Thailand DTA is one of the more expat-friendly treaties in Thailand's network, but its protections are highly specific to income category. The treaty does not grant blanket UK-only taxation on all income.

- UK Government / Civil Service Pensions (Article 19): Taxed exclusively in the UK. Thailand has no taxing rights. If you receive a UK civil service, NHS, military, or teacher's pension, you owe nothing to Thailand on that income, regardless of how much you remit.

- UK State Pension: Falls under the pensions article, generally taxable in Thailand as the country of residence. However, the relatively modest amounts (£11,500–£12,000/year for 2026) mean the Thai liability after allowances is often minimal.

- UK Private / Occupational Pensions: Thailand has taxing rights under the treaty, but at reduced treaty rates. These must be declared on a Thai PND 90/91 return.

- UK Dividends: Withholding tax capped at 15% (or 10% in certain cases) under the treaty. A Thai tax credit is available for UK tax already withheld.

- UK Rental Income: Generally taxable in the UK as the source country, with a credit mechanism in Thailand. Seek specialist advice on the interaction.

Australia: The Superannuation Grey Zone

The Australia–Thailand DTA was signed in 1989 — before Australia's modern superannuation system was fully established. The treaty text does not contain the word "superannuation." This is not a minor drafting oversight. It means there is no explicit treaty article governing how Australian super drawdowns are treated in Thailand.

The Thai Revenue Department has not issued a definitive public ruling on this. Practitioners are split. Some argue super distributions are "pensions" under the treaty's pension article and therefore receive treaty protection. Others argue the silence means they default to assessable income under Thai domestic law. Every Australian drawing down superannuation while a Thai tax resident is operating in genuine legal ambiguity.

For non-super income, the AUS–Thailand treaty provides:

- Australian Government Pensions (Article 19): Taxed exclusively in Australia. DVA pensions, federal public service pensions — these stay in Australia's taxing jurisdiction.

- Australian Dividends: Withholding capped at 15% under the treaty.

- Australian Interest: Withholding capped at 10%.

Germany: Strong Treaty, Complex Withholding

Germany's DTA with Thailand is comprehensive and generally well-structured for expat planning. However, Germany's domestic withholding tax system adds a layer of complexity that UK and Australian expats don't typically face.

- German State Pension (gesetzliche Rentenversicherung): Falls under treaty pension provisions. Germany often retains source-country taxing rights, and German authorities will withhold Quellensteuer (withholding tax) before the money leaves. Thai residents can apply for a Thai tax credit, but documentation requirements are significant.

- German Civil Service Pensions (Beamtenpension): Covered under Article 19-equivalent provisions — taxed in Germany, not Thailand.

- German Dividends: Withholding capped at 15% (5% if the recipient holds 25%+ of the company).

- Abgeltungsteuer (Capital Gains Withholding): Germany's flat 25% capital gains tax is deducted at source. Treaty interaction with Thai PIT on the same gain must be managed carefully to avoid double taxation without a full credit.

DTA Protection by Income Type: Country Comparison

| Income Type | 🇺🇸 USA (No DTA) | 🇬🇧 UK | 🇦🇺 Australia | 🇩🇪 Germany |

|---|---|---|---|---|

| Government / Civil Service Pension | Up to 35% Thai PIT | UK only (0% in Thailand) | AUS only (0% in Thailand) | Germany only (0% in Thailand) |

| Private / Occupational Pension | Up to 35% Thai PIT | Thailand taxing rights (treaty rate) | Thailand taxing rights (treaty rate) | Germany may retain rights; credit available |

| Superannuation / Equivalent | Up to 35% Thai PIT | N/A | Legally ambiguous (no treaty article) | N/A |

| Dividends | Up to 35% Thai PIT | Max 15% withholding; credit in Thailand | Max 15% withholding; credit in Thailand | Max 15% withholding; credit in Thailand |

| Interest | Up to 35% Thai PIT | Max 25% (often reduced) | Max 10% | Max 25% (often reduced) |

| Rental Income (overseas property) | Up to 35% Thai PIT | Source country primary; credit mechanism | Source country primary; credit mechanism | Source country primary; credit mechanism |

Worked Example: Same Income, Different Passports

Scenario: ฿2,400,000 remitted to Thailand in 2025 (all from private pension / retirement income)

Assumptions: Single filer, standard Thai personal allowance of ฿60,000 + expense deduction of 50% of pension income (capped at ฿100,000), no other Thai income. Net assessable income after deductions: approximately ฿2,240,000.

American (no DTA):

- ฿150,000 @ 0% = ฿0

- ฿150,000 @ 5% = ฿7,500

- ฿200,000 @ 10% = ฿20,000

- ฿250,000 @ 15% = ฿37,500

- ฿250,000 @ 20% = ฿50,000

- ฿1,000,000 @ 25% = ฿250,000

- ฿240,000 @ 30% = ฿72,000

- Total Thai PIT: ฿437,000 — with no treaty credit against US taxes paid

UK national (government / civil service pension under Article 19):

- Article 19 grants exclusive taxing rights to the UK. Thailand has zero taxing rights on this income.

- Total Thai PIT: ฿0

UK national (private occupational pension):

- Thailand has taxing rights. The same PIT calculation applies as the American scenario, but any UK tax already withheld at source generates a credit in Thailand. If UK withheld ฿180,000 equivalent, the net Thai liability reduces to approximately ฿257,000.

Australian (government pension under Article 19):

- Australia retains exclusive taxing rights. Total Thai PIT: ฿0

Australian (superannuation drawdown):

- No treaty article applies. Until the Revenue Department issues a ruling, treating this as fully assessable is the conservative (and defensible) approach. Thai PIT liability: up to ฿437,000 — identical to the American scenario.

How to Claim DTA Relief in Thailand

- Identify the specific article of the relevant DTA that covers your income type. Do not assume — read the treaty text or consult a specialist.

- Obtain documentation of foreign tax paid: withholding tax certificates, P60 (UK), PAYG summaries (Australia), Steuerbescheid (Germany).

- File a Thai PND 90 or PND 91 return by 31 March of the following year, declaring all assessable remitted income.

- Claim the foreign tax credit or treaty exemption on the return. If the treaty grants exclusive taxing rights to the other country, declare the income and annotate the exemption with the relevant DTA article citation.

- Retain all documentation for five years — the Thai Revenue Department's audit window.

Frequently Asked Questions

I'm American — is there anything I can do to reduce my Thai tax liability without a DTA?

Yes, though the options are domestic rather than treaty-based. Thailand's standard deductions and allowances (personal allowance, age allowance for over-65s, LTF/RMF fund contributions, insurance premiums) reduce your assessable income before PIT applies. Americans can also claim the US Foreign Tax Credit on their US return for Thai taxes paid — preventing double taxation at the US end, even if it doesn't reduce the Thai bill. Structural planning (e.g., timing of remittances, income type optimisation) should be discussed with a cross-border tax specialist familiar with both US and Thai systems.

Does my DTA automatically apply, or do I have to claim it?

You must actively claim treaty relief. Filing a Thai tax return and claiming the relevant DTA article is required — treaty protections are not applied automatically. Failure to file does not protect you; it simply creates a compliance risk on top of the underlying liability.

I receive both a UK government pension and a UK private pension. How does this work?

The two income streams are treated separately under the UK–Thailand DTA. Your government pension is exempt from Thai tax under Article 19 — declare it on your return but annotate the Article 19 exemption. Your private pension is assessable in Thailand; calculate PIT on that amount separately and claim credit for any UK tax already withheld. You will need to maintain separate documentation for each income stream.

I've heard the 183-day rule can be managed by leaving Thailand for short periods. Is this still viable?

The 183-day rule is a calendar-year cumulative count — it is not reset by leaving Thailand temporarily. If you spend 185 days total in Thailand across a calendar year (even with trips abroad in between), you are a Thai tax resident for that year. Genuine non-residency means spending fewer than 183 days in Thailand across the full calendar year. The Revenue Department has made clear it is scrutinising residency claims more closely for TY2024 onwards.

What is the filing deadline and what happens if I miss it?

The Thai PIT filing deadline is 31 March of the year following the tax year (TY2025 returns are due 31 March 2026). Online filing via the Revenue Department's e-filing portal extends this slightly in some years — check rd.go.th for the current year's position. Late filing attracts a surcharge of 1.5% per month on unpaid tax, plus a penalty of up to 100% of the tax due in serious cases. With active enforcement signalled for TY2024+, timely filing is not optional.

Action Steps

- Confirm your Thai tax residency status for 2025: count every day you were physically in Thailand across the calendar year.

- Identify every category of foreign income you remitted to Thailand in 2025 — pension, dividends, interest, rental, salary, capital gains — separately.

- Locate the specific DTA treaty article (if a DTA exists for your nationality) that covers each income type. Do not assume all income is covered the same way.

- Gather foreign tax documentation: withholding certificates, P60, PAYG summaries, or equivalent for the relevant tax year.

- Engage a Thai tax adviser with cross-border treaty experience before 31 March 2026 — not after. Treaty interpretation disputes are significantly harder to resolve post-filing.

- If you are Australian drawing superannuation, seek a specialist opinion on your specific fund and drawdown structure before remitting further funds.

- If you are American, begin exploring the US Foreign Tax Credit calculation with a US-licensed CPA familiar with expat tax to minimise double taxation at the US end.