Thailand Income Tax: Expat Guide to PIT Rates & Deductions

Two expats. Same Chiang Mai condo building. Same ฿960,000 remitted to Thailand in 2025. One owes ฿188,500 in Thai personal income tax. The other owes ฿0. The difference is not an offshore structure or aggressive tax avoidance — it is a single clause in a Double Tax Agreement and a correctly applied deduction stack. This guide walks through every variable that determines your Thai PIT bill in 2026: residency rules, the full bracket table, every major deduction, DTA Article 19 protection, filing deadlines, and the penalties for getting it wrong.

Who Is a Thai Tax Resident in 2026?

Thailand uses a simple physical-presence test: spend 180 days or more in Thailand during a calendar year and you are a Thai tax resident for that year. There is no domicile concept, no "centre of life" analysis, and no formal registration process. The threshold is 180 days — not 183, not 6 months as colloquially rounded. One additional day above 179 triggers full residency.

Thai tax residency has two consequences. First, you are liable to file a Thai personal income tax return (PND 90 or PND 91) if your assessable income exceeds ฿120,000 for a single filer or ฿220,000 for a married couple. Second, under Revenue Department Orders Por 161/2566 and Por 162/2566 — effective 1 January 2024 — all foreign-source income remitted to Thailand in the same tax year it was earned is assessable. The old planning technique of earning income in year one and remitting it in year two is no longer effective for income earned after 31 December 2023.

If you are below the 180-day threshold, you are a non-resident for Thai tax purposes. Non-residents are taxed only on Thailand-sourced income and at the same PIT rates, but most remittance-based expats will not qualify.

Thailand PIT Brackets 2026 (Net Taxable Income)

Thailand's personal income tax is progressive. The rates below apply to net taxable income — the figure remaining after all allowable deductions and DTA exemptions have been subtracted from gross assessable income. This distinction is critical: the 35% top rate almost never applies to gross remittances for a retiree who has correctly applied their deductions.

| Net Taxable Income (฿) | Tax Rate | Tax on Band (฿) | Cumulative Max Tax (฿) |

|---|---|---|---|

| ฿0 – ฿150,000 | 0% | 0 | 0 |

| ฿150,001 – ฿300,000 | 5% | 7,500 | 7,500 |

| ฿300,001 – ฿500,000 | 10% | 20,000 | 27,500 |

| ฿500,001 – ฿750,000 | 15% | 37,500 | 65,000 |

| ฿750,001 – ฿1,000,000 | 20% | 50,000 | 115,000 |

| ฿1,000,001 – ฿2,000,000 | 25% | 250,000 | 365,000 |

| ฿2,000,001 – ฿5,000,000 | 30% | 900,000 | 1,265,000 |

| ฿5,000,001 and above | 35% | — | — |

Key Deductions and Allowances for Expat Retirees

The deduction stack is where most expats leave money on the table. Thailand's Revenue Code allows a generous set of personal deductions that, when combined, can eliminate tax liability entirely for moderate remittances.

Standard Deductions

- Personal allowance: ฿60,000 (every Thai tax resident)

- Spouse allowance: ฿60,000 (if spouse has no income)

- Pension / employment income deduction: 50% of income, capped at ฿100,000 (applicable to pension income classified as income from employment under Section 40(1))

- Age 65+ allowance: ฿190,000 additional exemption for filers aged 65 or older

- Life insurance premiums: up to ฿100,000

- Health insurance premiums: up to ฿25,000

- Parents' health insurance: up to ฿15,000 per parent

- Thai Retirement Mutual Fund (RMF): up to 30% of income, max ฿500,000

- Charitable donations: up to 10% of net income after other deductions

Deduction Stack for a 65+ Retiree (Illustrative)

- Personal allowance: ฿60,000

- Age 65+ allowance: ฿190,000

- Pension income deduction (50%, capped): ฿100,000

- Spouse allowance (if applicable): ฿60,000

- Health/life insurance: up to ฿125,000

- Total potential deductions: ฿480,000 – ฿535,000+ before any DTA exemptions

Double Tax Agreements: The Variable That Changes Everything

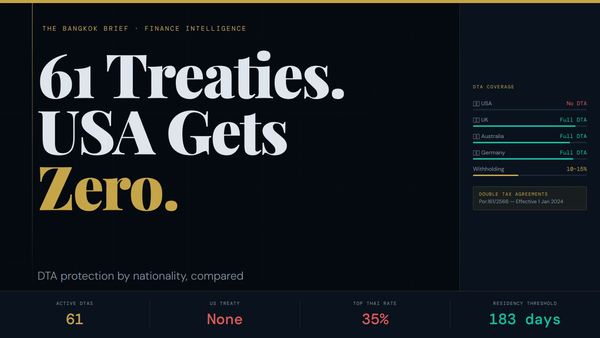

Thailand has Double Tax Agreements (DTAs) with 61 countries. These treaties override domestic Thai tax law for specific income types — meaning certain income is either exempt from Thai tax entirely, or taxed at a reduced rate. Your nationality and the source of your income determine which treaty provisions apply to you.

DTA Article 19: Government Service Pensions

Article 19 (Government Service) is the most powerful clause for retirees. Under most of Thailand's DTAs, pensions paid by a foreign government for services rendered to that government — including civil service pensions, military pensions, and most public-sector pensions — are taxable only in the country that paid them. Thailand has no taxing rights whatsoever over this income, regardless of how long the recipient stays in Thailand or how much is remitted.

This applies to: US federal civil service and military pensions (CSRS, FERS, military retirement pay), UK government and NHS pensions, Australian government pensions paid for public-sector service, and equivalents across most of Thailand's 61 DTA partners.

What Article 19 Does NOT Cover

- US Social Security (separate treatment — partially assessable in Thailand)

- US private 401(k) / IRA distributions

- UK private pensions and SIPPs

- Investment income (dividends, capital gains, rental income)

- Any income earned from private-sector employment

US–Thailand DTA: The Nuance Americans Must Understand

The United States does have a DTA with Thailand — but it is narrower than many expats assume. US government and civil service pensions under Article 19 are fully exempt from Thai tax. However, US Social Security, private pensions, 401(k) distributions, and IRA withdrawals do not receive the same protection and are treated as assessable income under Thai domestic law. Americans relying on private retirement accounts should budget for Thai PIT on remitted amounts after deductions.

Filing Deadlines and Penalties

| Filing Method | Deadline | Form | Platform |

|---|---|---|---|

| Paper filing | 31 March 2026 | PND 90 / PND 91 | Local Revenue Department office |

| e-Filing (online) | 8 April 2026 | PND 90 / PND 91 | rd.go.th |

The penalty for non-filing when assessable income exceeds the threshold is severe: 200% of the tax owed, plus 1.5% monthly interest on the outstanding amount. If your assessable income after deductions results in zero tax owed, you still have a technical filing obligation — though the practical penalty exposure is zero. When in doubt, file.

Worked Example: Two Expats, Same ฿960,000 Remittance

Expat A: US Government Retiree, Age 68, Single

Annual remittance to Thailand: ฿960,000 — entirely from a US federal civil service (FERS) pension.

- DTA Article 19 applies → entire ฿960,000 is exempt from Thai tax

- Net assessable income: ฿0

- Thai PIT owed: ฿0

Note: Expat A should still confirm with a Thai tax adviser whether a nil return filing is recommended for documentation purposes.

Expat B: US Private-Sector Retiree, Age 68, Single

Annual remittance to Thailand: ฿960,000 — from 401(k) distributions. No Article 19 protection applies.

- Gross assessable income: ฿960,000

- Less: pension income deduction (50%, capped at ฿100,000): −฿100,000

- Less: personal allowance: −฿60,000

- Less: age 65+ allowance: −฿190,000

- Net taxable income: ฿610,000

- Tax calculation:

- ฿0–฿150,000 @ 0% = ฿0

- ฿150,001–฿300,000 @ 5% = ฿7,500

- ฿300,001–฿500,000 @ 10% = ฿20,000

- ฿500,001–฿610,000 @ 15% = ฿16,500

- Total Thai PIT owed: ฿44,000

This is the realistic figure after proper deduction application — significantly lower than the ฿188,500 figure cited at the top, which represents a filer who has applied no deductions and remitted the same amount without any allowances. The contrast illustrates why knowing your deduction entitlements is not optional.

Expat C: Same as Expat B, Zero Deductions Applied (Common Mistake)

- Gross assessable income: ฿960,000

- No deductions claimed

- Tax on ฿960,000 gross:

- ฿0–฿150,000 @ 0% = ฿0

- ฿150,001–฿300,000 @ 5% = ฿7,500

- ฿300,001–฿500,000 @ 10% = ฿20,000

- ฿500,001–฿750,000 @ 15% = ฿37,500

- ฿750,001–฿960,000 @ 20% = ฿42,000

- Total Thai PIT owed: ฿107,000 — and rising toward ฿188,500 if additional income sources are included without deductions

Frequently Asked Questions

I've been in Thailand 185 days. Do I have to file even if I think I owe nothing?

If your assessable income exceeds ฿120,000 (single) or ฿220,000 (married), you are legally required to file a PND 90 or PND 91 return — even if deductions reduce your tax bill to zero. Failure to file when required triggers the 200% penalty on tax owed; if tax owed is zero, the penalty is zero, but the filing obligation still exists. File anyway to create a clean record with the Revenue Department.

Does my UK State Pension count as a government pension under Article 19?

No. The UK State Pension is a contributory social insurance benefit, not a payment for government service. It does not qualify for Article 19 exemption under the UK–Thailand DTA. It is assessable in Thailand after applicable deductions. UK government occupational pensions (civil service, NHS, military, teachers) do qualify under Article 19 and are exempt from Thai tax.

My income was earned before 2024. Is it still assessable if I remit it now?

Por 161/2566 and Por 162/2566 apply to income earned on or after 1 January 2024 that is remitted to Thailand. Income earned before 1 January 2024 and held offshore retains its pre-2024 treatment — it is not assessable when remitted, regardless of when the remittance occurs. Maintaining clear documentation of the year income was earned is now essential if you intend to remit pre-2024 savings.

Can I file in Thai baht even though my income is in USD or GBP?

Yes. All Thai tax returns are filed in Thai baht. The Revenue Department generally accepts the Bank of Thailand's average exchange rate for the relevant tax year for conversion purposes. Keep records of the exchange rate applied at each remittance point — your bank's SWIFT confirmation statements are the standard supporting document.

What is the difference between PND 90 and PND 91?

PND 91 is for filers whose only income is from employment (Section 40(1) — salary, wages, pension). PND 90 covers all other income types or mixed income. Most expats with foreign pensions, investment income, or rental income will file PND 90. If you are unsure, PND 90 is the safer default — it encompasses all income categories.

Action Steps for Thai Expat Filers in 2026

- Determine your residency status: Count your days in Thailand for calendar year 2025. If you reached 180 days, you are a Thai tax resident and the following steps apply.

- Classify every income source: Separate government-service pensions (potential Article 19 exemption) from private pensions, Social Security, investment income, and rental income. Each category has different DTA and domestic law treatment.

- Identify your applicable DTA: Check Thailand's DTA with your home country at rd.go.th. Locate the specific articles covering your income types — do not assume all income is protected equally.

- Calculate your full deduction stack: Personal allowance (฿60,000) + age-65+ allowance if applicable (฿190,000) + income-type deduction + spouse allowance + insurance premiums. Total your deductions before calculating any tax.

- Run your net taxable income through the bracket table: Apply the progressive rates to the net figure, not your gross remittance. The difference is often tens of thousands of baht.

- File by the deadline: Paper returns by 31 March 2026 at your local Revenue Department office. e-Filing via rd.go.th by 8 April 2026. Prepare your TIN (Tax Identification Number) in advance — apply at any Revenue Department office with your passport if you don't have one.

- Retain all documentation for five years: Bank statements showing remittance dates and amounts, exchange rate records, pension statements, and DTA claim documentation. The Revenue Department's assessment window is five years from the filing deadline.