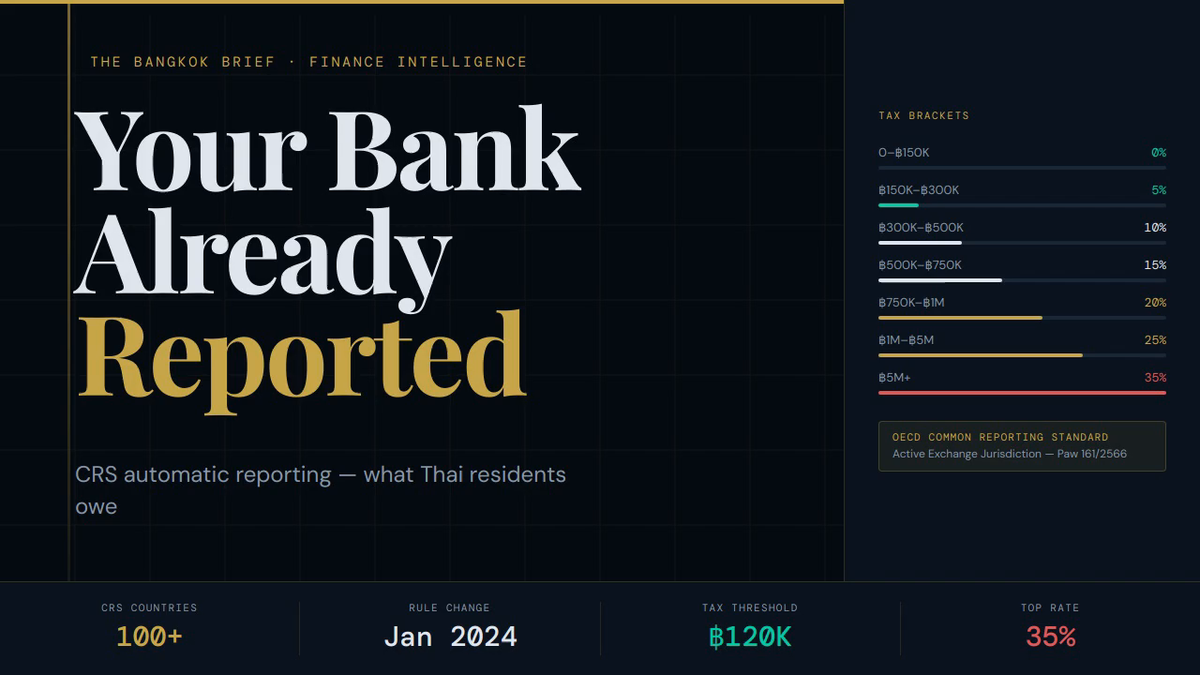

Thailand CRS: Your Overseas Accounts Are Being Reported

If you are a foreign national living in Thailand for more than 180 days a year and remitting income from overseas, your financial data is already being exchanged between governments — automatically, annually, and without any notification to you. Thailand is an active participant in the OECD Common Reporting Standard (CRS), and a landmark rule change effective 1 January 2024 under Revenue Department Instruction Paw 161/2566 means that foreign income remitted to Thailand in the same calendar year it is earned is now fully taxable. The old one-year deferral strategy is dead. If you have not yet assessed your Thai tax position, you may already have an outstanding liability.

What Is CRS and How Does It Work?

The Common Reporting Standard is an OECD framework for automatic government-to-government financial data exchange. Adopted by over 100 jurisdictions — including the UK, Australia, Canada, the European Union, Singapore, and the UAE — CRS requires financial institutions to identify account holders who are tax residents of another participating country, compile a standardised report on those accounts, and transmit it to their domestic tax authority, who then forwards it to the relevant foreign government.

There is no audit trigger, no warrant requirement, and no warning sent to the account holder. The exchange happens once per year, covering the prior calendar year's data.

What Information Is Reported Under CRS

- Full legal name

- Tax Identification Number (TIN) — including your Thai TIN if you have one

- Date of birth and address on file

- Account number and institution name

- Year-end account balance

- Total interest earned

- Total dividends received

- Gross proceeds from the sale of financial assets

Critically, the report flows in both directions. Your home country receives data about your Thai accounts. Thailand receives data about your overseas accounts held at institutions in other CRS-participating countries. This is the compliance pincer that now traps undisclosed expat income from two angles simultaneously.

Thailand's CRS Status and the Paw 161/2566 Rule Change

Thailand formally activated automatic exchange of information under CRS in 2023, with Thailand being treated as an active exchange jurisdiction as of 2025. This coincided with — and reinforced — a separate but equally significant domestic tax change.

Prior to 1 January 2024, Thai Revenue Department guidance allowed a practical workaround: if you earned foreign income in Year 1 but did not remit it to Thailand until Year 2, that income was not subject to Thai personal income tax. Expats used this deferral strategy routinely, parking income offshore for one calendar year before bringing it in.

Revenue Department Instruction Paw 161/2566, effective 1 January 2024, eliminated this loophole. Under the new rule, any foreign-sourced income remitted to Thailand in the same calendar year it is earned is assessable income for Thai tax purposes — regardless of which bank account it passes through or how it is structured.

| Period | Rule | Tax Outcome for Remitted Foreign Income |

|---|---|---|

| Before 1 Jan 2024 | One-year deferral allowed | Defer income to Year 2 → effectively tax-free in Thailand |

| From 1 Jan 2024 | Paw 161/2566 in force | Same-year remittance = taxable assessable income |

Thai Tax Residency: The 180-Day Trigger

Thai personal income tax applies to individuals who are tax resident in Thailand, defined as spending 180 or more days in Thailand within a single calendar year. This threshold is cumulative, not consecutive — weekends in Bangkok count the same as months in Chiang Mai.

If you cross the 180-day threshold, you are required to:

- Obtain a Thai Tax Identification Number (TIN) from your local Revenue Department office

- File a Thai personal income tax return (Form PND 90) by 31 March of the following year (or 8 April for online filing)

- Declare all foreign-sourced income remitted to Thailand during the tax year

Thai tax law does not automatically assess you — you self-declare. But CRS means the Revenue Department may already have data points to cross-reference against what you file (or don't file).

Thai Personal Income Tax Brackets (2025)

| Assessable Income (฿) | Tax Rate | Tax on Band (฿) |

|---|---|---|

| 0 – 150,000 | 0% | 0 |

| 150,001 – 300,000 | 5% | Up to 7,500 |

| 300,001 – 500,000 | 10% | Up to 20,000 |

| 500,001 – 750,000 | 15% | Up to 37,500 |

| 750,001 – 1,000,000 | 20% | Up to 50,000 |

| 1,000,001 – 2,000,000 | 25% | Up to 250,000 |

| 2,000,001 – 5,000,000 | 30% | Up to 900,000 |

| Above 5,000,000 | 35% | On the excess |

The filing obligation triggers at ฿120,000 per year (~$3,300 USD at current exchange rates) in assessable income for single filers. Below this threshold, no return is legally required — but it is still worth obtaining a TIN and documenting your position.

Worked Example: Expat Remitting $60,000 USD to Thailand

Assume a British national living in Bangkok on a Thailand Elite visa, spending 210 days per year in Thailand, and remitting $60,000 USD (~฿2,160,000 at ฿36/USD) in foreign employment income during the 2024 tax year.

Step 1 — Determine Thai assessable income

Gross remittance: ฿2,160,000

Standard employment income deduction (50%, capped at ฿100,000): − ฿100,000

Personal allowance: − ฿60,000

Assessable income: ฿2,000,000

Step 2 — Calculate tax on ฿2,000,000 assessable income

- ฿0 – ฿150,000: 0% = ฿0

- ฿150,001 – ฿300,000: 5% = ฿7,500

- ฿300,001 – ฿500,000: 10% = ฿20,000

- ฿500,001 – ฿750,000: 15% = ฿37,500

- ฿750,001 – ฿1,000,000: 20% = ฿50,000

- ฿1,000,001 – ฿2,000,000: 25% = ฿250,000

Total Thai income tax liability (before DTA): ฿365,000 (~$10,138 USD)

Step 3 — Apply the UK–Thailand Double Tax Agreement

The UK–Thailand DTA allows UK-sourced employment income taxed in the UK to be credited against Thai tax liability. If the individual paid £8,000 (~฿370,000) in UK income tax on the same income, this credit can eliminate the Thai liability entirely — but only if a PND 90 return is filed and the DTA credit is formally claimed. Without filing, the credit is forfeited and the full ฿365,000 remains due, plus potential penalties.

Double Tax Agreements: What They Do and Don't Do

Thailand has active Double Tax Agreements (DTAs) with over 60 countries, including the UK, Australia, Canada, Germany, France, Japan, and Singapore. DTAs generally prevent the same income from being taxed twice by allocating taxing rights between the two countries.

However, DTAs do not:

- Automatically zero out your Thai tax bill

- Apply if you fail to file a Thai return

- Override Thai domestic law unless correctly invoked

- Cover all income types equally — dividend withholding rates, for example, vary by agreement

The correct process is to file a Thai PND 90 return, declare the relevant income, attach supporting documentation of foreign tax paid, and formally claim the DTA credit or exemption. A qualified Thai tax adviser can prepare this filing; expect fees of ฿5,000–฿30,000 depending on complexity.

Frequently Asked Questions

I've been in Thailand for years and never filed a Thai tax return. Am I in trouble?

Potentially, yes — particularly for tax years 2024 onward when Paw 161/2566 came into force. Thai statute of limitations for tax assessment is generally two years from the filing deadline for standard cases, rising to five years if the Revenue Department initiates an inquiry. Voluntary disclosure before any audit is always treated more favourably than being caught. If you have been remitting foreign income and spending 180+ days in Thailand, consult a Thai tax adviser promptly.

My money never actually entered a Thai bank account — it was sent to my foreign account and I used a debit card in Thailand. Am I still liable?

The Thai Revenue Department's position is that income is "remitted" when it is brought into Thailand and used for living expenses there, regardless of the precise mechanism. Using a foreign debit card to withdraw baht from ATMs or pay for goods and services in Thailand is considered remittance by most Thai tax advisers interpreting Paw 161/2566. This remains an area of active interpretation, and specialist advice is recommended.

I only have a tourist visa. Does Thai tax residency still apply?

Yes. Tax residency in Thailand is determined solely by physical presence — 180 days per calendar year — not by visa type. Tourist visa holders, ED visa holders, retirement visa holders, and Elite card holders are all subject to the same 180-day rule. There is no visa category that automatically exempts you from Thai tax residency.

Does CRS apply to cryptocurrency wallets and offshore broker accounts?

CRS currently applies to accounts held at financial institutions — banks, brokers, and certain custodians. Pure cryptocurrency wallets held in self-custody are not reportable under current CRS rules. However, centralised exchanges (Binance, Coinbase, Kraken, etc.) that are registered in CRS-participating jurisdictions are required to report account holders. This area is evolving rapidly; several jurisdictions are extending CRS-equivalent frameworks to crypto asset service providers from 2026 onward.

What is the penalty for failing to file a Thai PND 90 return?

Late filing incurs a surcharge of 1.5% per month on any tax due, plus a one-time penalty of up to 100% of the tax liability if the Revenue Department issues an assessment. If you file voluntarily before receiving any Revenue Department notice, penalties are typically reduced significantly. There is no criminal liability for first-time, good-faith non-compliance — but repeated failures or intentional evasion can escalate.

Action Steps

- Determine your 2024 day count. Review your passport stamps and travel records. If you spent 180+ days in Thailand in 2024, you were a Thai tax resident for that year.

- Identify all foreign income remitted to Thailand in 2024. Include bank transfers, ATM withdrawals using foreign cards, and any asset proceeds brought into Thailand.

- Obtain a Thai TIN from your local Revenue Department district office if you do not already have one. Bring your passport and proof of address.

- Check whether your home country has a DTA with Thailand and identify which income types are covered. The Thai Revenue Department publishes the full list of DTAs at rd.go.th.

- Engage a qualified Thai tax adviser experienced in expat PND 90 filings. File your return by 31 March (paper) or 8 April (online) for the preceding tax year.

- Update your address on file with your home-country bank to ensure CRS reports are accurate and consistent with your filed tax positions in both jurisdictions.

- Subscribe to The Bangkok Brief newsletter at thebangkokbrief.com for updates on how Paw 161/2566 interacts with specific visa categories, DTA guidance, and future Revenue Department instructions.