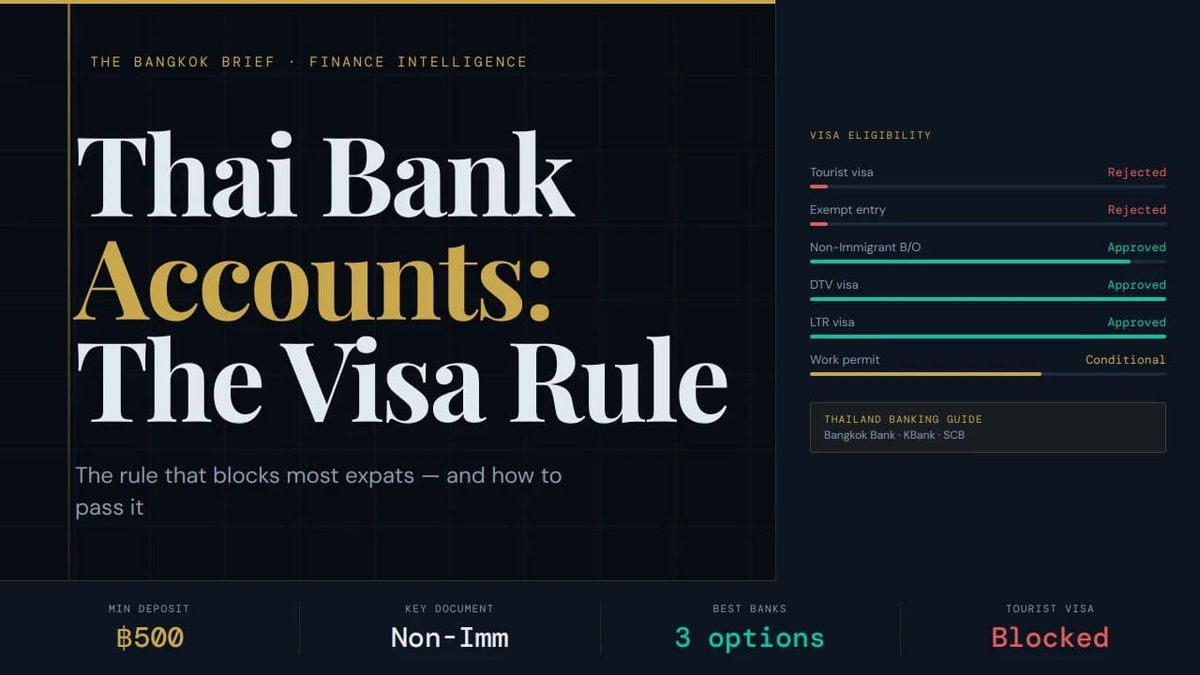

Thailand Bank Account: The Visa Rule That Blocks Most Expats

Opening a Thai bank account in 2025 costs as little as ฿500 (~$14 USD) — but the deposit is almost irrelevant. The factor that determines whether you walk out with an account or a polite rejection is the visa category stamped in your passport. Most expat guides focus on document checklists and miss this entirely. This article covers exactly which visas work, which branches accept foreigners, what the complete document stack looks like, how the fee structures compare across Thailand's major banks, and the one workaround that works when your visa isn't ideal.

Why Thai Banks Reject Most Foreigners on the First Visit

Between 2022 and 2023, Thai commercial banks quietly tightened their account-opening policies for foreign nationals. The change was never announced publicly — it was implemented branch-by-branch through internal compliance guidance. The practical result: walk into most standard branches on a tourist visa or visa-exempt entry today, and the probability of being turned away exceeds 90%.

This isn't arbitrary. Thai banks operate under Anti-Money Laundering Office (AMLO) guidelines that require demonstrable proof of legitimate, ongoing residency. A tourist visa, by definition, signals temporary presence. Banks have no incentive to take on compliance risk for a customer who may leave in 30 days. The branches that do open accounts for tourists tend to be specialist foreigner-facing desks — and even those have tightened significantly.

The solution is not to find a friendlier teller. The solution is to arrive with the right visa.

Visa Types and Account Opening Likelihood

The table below reflects real-world success rates reported by expats and confirmed by branch staff at major banks as of 2025. These are approximate probabilities, not guarantees — individual branch managers retain discretion.

| Visa Type | Account Opening Likelihood | Notes |

|---|---|---|

| Tourist Visa (TR) | ~10% | Almost always refused at standard branches; specialist desks only |

| Visa Exempt (30-day stamp) | ~5% | Effectively impossible at most banks in 2025 |

| Non-Immigrant B (Work) | ~85% | Strong baseline; work permit strengthens application further |

| Non-Immigrant O (Retirement/Family) | ~85% | Widely accepted; must show proof of income or funds |

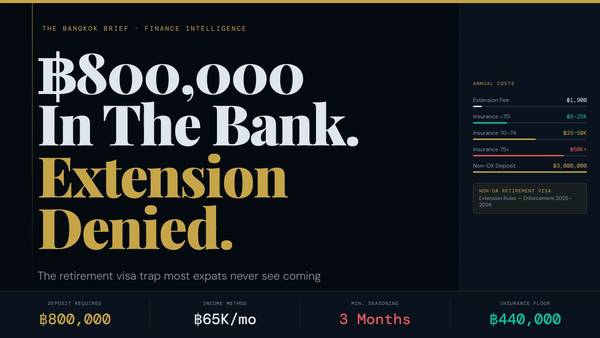

| Non-Immigrant OA (Long-Stay Retirement) | ~90% | Easiest category; proof of ฿800,000 in home bank typically required for visa anyway |

| DTV (Destination Thailand Visa) | ~75% | New 2024 visa; requires ฿500,000 proof of funds; banks increasingly recognise it |

| LTR Visa (10-year) | ~95% | Highest-tier visa; banks treat holders as premium customers |

| Education Visa (ED) | ~40% | Inconsistent; language school ED visas viewed sceptically |

The Complete Document Stack

Arriving with a complete document set dramatically increases your success rate even at branches that are borderline on your visa type. Missing a single original document is the most common reason for same-day rejections.

- Passport: Original required — no photocopies accepted as a substitute. Bring 2–3 photocopies of the photo page, visa page, and entry stamp for the bank to keep on file.

- Visa: The current valid visa page. If you have a Non-Immigrant visa, ensure it has not expired and that your most recent entry stamp is visible.

- Proof of address in Thailand: Rental contract (most common), utility bill in your name, or a letter from your landlord. Some branches accept a hotel booking for recent arrivals, but this is increasingly rare.

- Embassy Resident Certificate: Issued by your home country's embassy in Bangkok. Costs vary by embassy (typically ฿300–฿1,500 and 1–5 business days). Thai banks accept this as supplementary evidence of residency. This is the critical workaround for visa categories with low baseline success rates.

- Work Permit (if applicable): Not required, but significantly strengthens applications for Non-B holders. Bring the original.

- Initial deposit: The minimum varies by bank and account type (see fee table below), but ฿500–฿2,000 in cash covers every standard savings account.

The Embassy Resident Certificate Workaround

This is the most underused tool in an expat's banking toolkit. If you're on a visa category with low success odds — or you're between visas — your home country embassy in Bangkok can issue a document certifying that you are a registered national residing in Thailand. Thai bank compliance officers accept this as evidence of legitimate, stable residency.

The process: contact your embassy directly (most have a consular services page), bring your passport, complete a short form, pay the fee, and collect within the stated timeframe. The US Embassy, UK Embassy, Australian Embassy, and most European embassies all offer this service. Some embassies allow walk-in appointments; others require advance booking.

Combined with a tourist visa or even a recent extension stamp, this document has successfully opened accounts at Bangkok Bank Silom, KBank, and SCB branches that would otherwise have declined.

Bank-by-Bank Comparison: The Major Players in 2025

| Bank | Foreigner Friendliness | Best Branch for Expats | Mobile App (English) | Minimum Deposit | Monthly Fee |

|---|---|---|---|---|---|

| Bangkok Bank | ★★★★★ | Silom HQ (dedicated English desk) | Bualuang mBanking — functional English | ฿500 | ฿0 |

| Kasikorn Bank (KBank) | ★★★★☆ | Asok / Siam Paragon branches | KPlus — rated #1, full English | ฿2,000 | ฿0–฿50 |

| SCB (Siam Commercial Bank) | ★★★☆☆ | SCB Park Plaza (head office area) | SCB Easy — good English support | ฿2,000 | ฿0 |

| Krungsri (Bank of Ayudhya) | ★★★☆☆ | Central World / Centralised branches | KMA — partial English | ฿1,000 | ฿0 |

| Krungthai Bank (KTB) | ★★☆☆☆ | Large city-centre branches only | Krungthai NEXT — limited English | ฿1,000 | ฿0 |

Bottom line: Bangkok Bank Silom is the single best branch in Thailand for first-time expat account opening. KBank wins on mobile banking experience once you're set up. Most expats end up holding accounts at both.

The Real Cost of Not Having a Thai Bank Account

Every foreign card ATM withdrawal in Thailand incurs a ฿220 flat fee charged by the Thai ATM network — this is unavoidable regardless of which overseas bank you use. On top of that, your home bank typically applies a 3–5% foreign exchange spread on the transaction. On a single ฿3,000 cash withdrawal, you could be paying:

- ฿220 flat ATM fee = 7.3% on a ฿3,000 withdrawal

- 3–5% FX spread from your home bank = ฿90–฿150 additional

- Total cost: ฿310–฿370 on a ฿3,000 withdrawal = up to 12.3%

For an expat withdrawing ฿30,000/month in cash, that's ฿3,100–฿3,700 lost annually to fees alone — enough to cover a month of groceries in Bangkok. A local Thai bank account eliminates the ATM fee entirely for domestic withdrawals and removes the FX spread on funds transferred in via services like Wise or Revolut.

The DTV Visa: 2025's New Banking Wildcard

The Destination Thailand Visa (DTV), introduced in mid-2024, is designed for remote workers, freelancers, and long-stay travellers. It requires proof of ฿500,000 (~$14,000 USD) in accessible funds — a higher bar than a standard tourist visa, but far lower than the LTR visa thresholds.

Thai banks are still calibrating their policies around DTV holders. As of early 2025, Bangkok Bank Silom and several KBank city-centre branches have confirmed they will open accounts for DTV holders with a full document stack. Expect this to become standard practice across all major banks by mid-2025 as the visa cohort grows.

Example: What a Complete Application Actually Looks Like

Scenario: British national, 38 years old, Non-Immigrant O visa (retirement extension), applying at Bangkok Bank Silom

- Documents prepared: Passport original + 3 photocopies (photo page, visa page, latest entry stamp), Non-O visa page copy, rental contract for condo in Sukhumvit (12-month lease, signed), embassy resident certificate from British Embassy Bangkok (collected 2 days prior, cost: ฿500), ฿2,000 cash for initial deposit.

- Branch selection: Bangkok Bank Silom HQ, 2nd floor English desk — not the ground floor standard queue. Arrived at 10:00 AM on a Tuesday (avoid Monday mornings and Friday afternoons — highest wait times).

- Process time: Approximately 45–60 minutes including form completion, document verification, and card issuance.

- Account opened: Basic savings account with Bangkok Bank. Passbook issued same day. Debit card issued same day or mailed within 5 business days depending on branch policy.

- Next step: Download Bualuang mBanking app, register with account number and Thai mobile SIM. Enable PromptPay linking with passport number for instant transfers.

Total cost to open: ฿2,000 deposit (remains yours) + ฿500 embassy certificate = ฿2,500 all-in. Monthly maintenance: ฿0.

Fee Structure: What Banks Don't Advertise

| Fee Type | Bangkok Bank | KBank | SCB |

|---|---|---|---|

| Monthly maintenance | ฿0 | ฿0–฿50 | ฿0 |

| Domestic ATM withdrawal (own network) | ฿0 | ฿0 | ฿0 |

| Domestic ATM withdrawal (other network) | ฿10–฿20 | ฿10–฿20 | ฿10–฿20 |

| International wire transfer (inbound) | ฿200 + 0.25% (max ฿500) | ฿200 + 0.25% (max ฿500) | ฿200 flat |

| PromptPay transfer | ฿0 | ฿0 | ฿0 |

| Savings interest rate (2024) | 0.5–1.0% p.a. | 0.5–1.5% p.a. | 0.5–1.0% p.a. |

Note: Thailand's real interest rate was 3.55% (World Bank, 2024). Standard savings accounts do not keep pace with inflation — consider a fixed deposit account for larger balances if you plan to hold significant baht long-term.

Frequently Asked Questions

Can I open a Thai bank account on a tourist visa?

Technically yes, practically almost never at standard branches in 2025. Your best option is Bangkok Bank Silom's dedicated expat desk combined with an embassy resident certificate. Even then, success is not guaranteed. If you have any flexibility, upgrade to a Non-Immigrant visa before attempting to open an account — it will save you multiple wasted trips.

Do I need a Thai phone number to open an account?

Yes. All Thai banks require a Thai mobile number for OTP (one-time password) verification during account setup and for mobile banking registration. Buy a Thai SIM before going to the bank — AIS, DTAC (now True Move), and True Move all sell tourist and long-stay SIMs at airports and 7-Eleven stores for ฿50–฿300.

Can I open a Thai bank account without a Thai address?

Most banks require a Thai address. If you're in a hotel, some branches accept a hotel booking confirmation for the short term, but this is increasingly rejected. A short-term rental contract (even 1–3 months) is a far stronger document. Serviced apartment contracts are widely accepted.

What's the best bank for receiving international transfers into Thailand?

Bangkok Bank has the most established international wire infrastructure and is widely supported by overseas banks. For Wise and Revolut transfers, KBank's account details are also well-supported. If you're receiving regular foreign income (relevant under the 2024 Por.161 tax rules), confirm with your bank that the account type supports inbound international transfers — some basic savings accounts have restrictions.

Will having a Thai bank account affect my tax obligations?

Having a Thai bank account itself does not trigger tax obligations. What matters is your tax residency status (180+ days in Thailand in a calendar year) and whether you are remitting assessable foreign income under Por.161/2566, which took effect 1 January 2024. A Thai bank account is the conduit — it doesn't create the liability, but it does create a paper trail. If you are a Thai tax resident, ensure you understand what funds you are remitting and whether they are assessable. Consult a Thai tax professional if in doubt.

Action Steps: How to Open Your Thai Bank Account in 2025

- Secure the right visa first. Non-Immigrant O, Non-B, Non-OA, DTV, or LTR all give you a strong baseline. Do not waste time attempting account opening on a tourist visa or visa-exempt entry unless you are using Bangkok Bank Silom specifically and have the full document stack.

- Get a Thai SIM card. Buy before your bank visit — you'll need it for OTP during the application. AIS and True Move are available at every major airport and at 7-Eleven.

- Obtain an embassy resident certificate if your visa is borderline. Allow 2–5 business days. Check your embassy's consular services page for current fees and booking procedures.

- Prepare your complete document stack in advance. Passport original, 3 photocopies of key pages, current visa, proof of Thai address, resident certificate, and ฿2,000 cash for deposit.

- Choose Bangkok Bank Silom for your first attempt if you're in Bangkok. Go to the dedicated English-speaking desk on arrival. Aim for mid-morning on a Tuesday, Wednesday, or Thursday.

- Register for mobile banking immediately after account opening. For KBank, download KPlus — it's the strongest English-language banking app in Thailand. Link your account to PromptPay using your passport number for instant domestic transfers.

- Review your remittance strategy. Under the 2024 Por.161 rules, all foreign income remitted to Thailand is potentially assessable if you are a tax resident. Use Wise or a similar service to transfer funds efficiently, and keep records of what you are bringing in and its source.