Por.161/2566: How Thailand Taxes Your Foreign Income Now

https://www.youtube.com/watch?v=PJD5S6EOf3Y

As of 1 January 2024, every foreign-sourced remittance you transfer into Thailand is potentially subject to Thai Personal Income Tax (PIT) — not just income earned in Thailand. This is the core consequence of Revenue Department Instruction Por.161/2566, issued quietly in September 2023. If you are a tax resident of Thailand (present 180 or more days in the calendar year) and you transfer money from an overseas bank account, the Thai Revenue Department now expects you to declare and potentially pay tax on that money. The loophole that allowed expats to defer foreign earnings indefinitely and remit them tax-free has been permanently closed.

What Por.161/2566 Actually Says

Por.161/2566 is a two-page administrative instruction that reinterprets Section 41 of the Thai Revenue Code. Section 41 has always stated that Thai tax residents owe PIT on foreign-sourced income brought into Thailand. For decades, however, the Revenue Department's informal interpretation allowed residents to wait until the calendar year after earning the income before remitting it — making that remittance technically "savings" and therefore untaxable.

Por.161 eliminated that calendar-year deferral. Under the new interpretation:

- Foreign income remitted to Thailand in any tax year from 2024 onward is assessable, regardless of when it was earned — unless it was earned before 1 January 2024 (see Por.162 below).

- The obligation applies to all Thai tax residents — any individual physically present in Thailand for 180 days or more in a calendar year, irrespective of visa type, nationality, or work permit status.

- The income must be declared on PND.90 or PND.91, Thailand's annual personal income tax return forms.

The Rule That Changed: The Old Loophole vs. The New Reality

To understand the magnitude of this change, consider how the old system worked versus how it works now:

| Scenario | Before Por.161 (pre-2024) | After Por.161 (2024 onward) |

|---|---|---|

| Earn ฿500,000 abroad in 2022, remit in 2023 | Tax-free — different calendar year | N/A (pre-2024 earnings still exempt via Por.162) |

| Earn ฿500,000 abroad in 2024, remit in 2024 | Would have been taxable (same year) | Taxable — declare on PND.90/91 |

| Earn ฿500,000 abroad in 2024, remit in 2025 | Would have been tax-free (different year) | Taxable — loophole is closed |

| Remit pre-2024 savings accumulated over many years | Tax-free | Still tax-free under Por.162/2566 — permanently exempt |

The 180-Day Residency Threshold

Por.161 does not create a new residency test — it relies on the existing Section 41 threshold. You become a Thai tax resident if you are physically present in Thailand for 180 days or more in any calendar year (1 January – 31 December). Key points:

- Days do not need to be consecutive. Any combination of stays totalling 180 days triggers residency.

- There is no minimum income, no work permit requirement, and no long-term resident visa requirement — presence alone is the test.

- Short trips abroad do not "reset" the count. Days in Thailand are cumulative within the tax year.

- If you spend fewer than 180 days in Thailand in a given year, you are a non-resident and Por.161 does not apply to your foreign remittances for that year.

Thai Personal Income Tax Brackets (2024)

Once foreign remittances are deemed assessable income, they are taxed at Thailand's standard progressive PIT rates. These rates apply to your net assessable income after allowable deductions (personal allowance, spouse allowance, child allowances, health insurance premiums, etc.).

| Net Assessable Income (THB) | Tax Rate | Tax on Band | Cumulative Tax |

|---|---|---|---|

| 0 – 150,000 | 0% | ฿0 | ฿0 |

| 150,001 – 300,000 | 5% | ฿7,500 | ฿7,500 |

| 300,001 – 500,000 | 10% | ฿20,000 | ฿27,500 |

| 500,001 – 750,000 | 15% | ฿37,500 | ฿65,000 |

| 750,001 – 1,000,000 | 20% | ฿50,000 | ฿115,000 |

| 1,000,001 – 2,000,000 | 25% | ฿250,000 | ฿365,000 |

| 2,000,001 – 5,000,000 | 30% | Up to ฿900,000 | Up to ฿1,265,000 |

| Above 5,000,000 | 35% | — | — |

Worked Example: $80,000 USD Remitted in 2024

Let's walk through exactly what a single expat with no dependants and standard deductions would owe if they remit $80,000 USD to Thailand in 2024.

Step 1 — Convert to THB

At mid-2024 exchange rates of approximately ฿36.25 per USD, $80,000 ≈ ฿2,900,000.

Step 2 — Apply Standard Deductions

Thailand allows an expense deduction of 50% of assessable income (capped at ฿100,000) for employment income, plus a personal allowance of ฿60,000. For simplicity, using a combined deduction of ฿160,000 (personal allowance + ฿100,000 expense deduction cap):

- Gross assessable remittance: ฿2,900,000

- Less deductions: −฿160,000

- Net assessable income: ฿2,740,000

Step 3 — Apply Progressive Tax Bands

- ฿0 – ฿150,000 @ 0% = ฿0

- ฿150,001 – ฿300,000 @ 5% = ฿7,500

- ฿300,001 – ฿500,000 @ 10% = ฿20,000

- ฿500,001 – ฿750,000 @ 15% = ฿37,500

- ฿750,001 – ฿1,000,000 @ 20% = ฿50,000

- ฿1,000,001 – ฿2,000,000 @ 25% = ฿250,000

- ฿2,000,001 – ฿2,740,000 @ 30% = ฿222,000

Total Thai PIT liability before DTA credits: ฿587,000 (~$16,193 USD)

Step 4 — Apply DTA Relief

If you are a US citizen, the US-Thailand DTA and US Foreign Tax Credit rules may allow you to offset some or all of this liability against US taxes already paid. The net liability depends entirely on your DTA country and income type. A licensed Thai tax adviser is essential at this income level.

Por.162/2566 — The Pre-2024 Savings Exemption

Issued alongside Por.161, Por.162/2566 is the permanent exemption for foreign income earned before 1 January 2024. Money accumulated in overseas accounts before that date can be remitted to Thailand at any time, in any amount, with zero Thai PIT liability. This is not a time-limited amnesty — it is a permanent carve-out.

Practical requirements to use Por.162:

- Maintain clear, dated bank statements showing the funds existed in your overseas account before 1 January 2024.

- Keep a separate account for pre-2024 savings and post-2024 income — commingling funds makes it nearly impossible to prove the source date.

- Retain payslips, investment statements, or other source documents to corroborate the earnings date if audited.

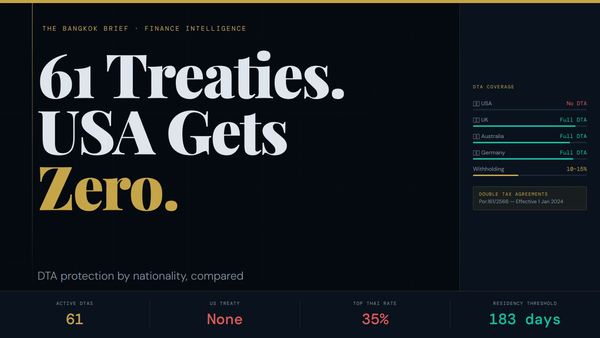

Double Taxation Agreements (DTAs)

Thailand has active DTAs with approximately 61 countries, including the USA, UK, Australia, Germany, France, and Canada. A DTA can:

- Exempt certain income types from Thai tax entirely (e.g., government pensions are often taxable only in the country of origin).

- Provide a tax credit for foreign taxes already paid, reducing your Thai liability dollar-for-dollar up to the Thai tax amount.

- Assign taxing rights — some DTAs give Thailand the right to tax, others give the source country the exclusive right.

DTA benefits are not automatic — you must claim them on your Thai return and provide documentation (e.g., foreign tax certificates). The applicable DTA and income type (employment, pension, dividends, capital gains, rental) determine your outcome dramatically. There is no single answer that applies to all expats.

Filing Deadlines and Obligations

| Filing Method | Deadline | Form | Filing Threshold |

|---|---|---|---|

| Paper return | 31 March | PND.90 (general) / PND.91 (employment) | Assessable income > ฿60,000 (single) or ฿120,000 (married) |

| e-Filing (online) | 8 April | PND.90 / PND.91 via rd.go.th | Same as above |

Note: If your total assessable income after deductions results in zero tax payable, you may still be required to file if your gross remittances exceed the threshold. Filing also creates a documented record that may protect you if the Revenue Department queries transfers from your Thai bank.

Smart Expat Responses to Por.161

- Ringfence pre-2024 savings now. Move funds earned before 1 January 2024 into a clearly labelled, dedicated account. Never mix with 2024+ earnings.

- Count your days carefully. If you are close to 180 days, a short trip abroad in December could make you a non-resident for that year — legally eliminating your Por.161 obligation for that tax year.

- Check your DTA. Look up your home country's DTA with Thailand and identify which income types it covers. The Revenue Department's English-language DTA database is available at rd.go.th.

- Get a Thai Tax Identification Number (TIN). You cannot file a PND.90 without one. Obtain it from your local Revenue Department district office.

- Consider income timing. If you control when you receive income (e.g., freelance payments, investment drawdowns), structuring remittances across multiple tax years can reduce the amount hitting higher brackets in any single year.

- Engage a Thai tax adviser. This is not optional at meaningful income levels. Adviser fees are typically ฿5,000–฿30,000 per year — trivial against potential penalties for non-compliance or overpayment from missing DTA credits.

Frequently Asked Questions

I only remit money to cover living expenses — does Por.161 still apply?

Yes. The Revenue Department does not distinguish between remittances for living expenses and remittances for investment. If the money originates from foreign-sourced income earned after 1 January 2024 and you are a Thai tax resident, it is assessable income regardless of what you spend it on in Thailand.

I'm retired and living off savings I built over 20 years. Am I affected?

Potentially not — if those savings were accumulated before 1 January 2024, Por.162 permanently exempts them. The critical step is proving the funds pre-date 2024. If you've been adding to those savings after 1 January 2024 (e.g., ongoing pension payments, investment returns), you need to segregate and document carefully.

My home country already taxes my income. Will I be taxed twice?

Not necessarily, but it depends on your DTA. Most DTAs contain provisions that either exempt the income from Thai tax or provide a credit for foreign taxes paid. The US, for example, has a DTA with Thailand that covers many income types, and US citizens can often use the Foreign Tax Credit to offset. However, the mechanics differ by income type and must be worked through with a qualified adviser.

What happens if I don't file? What are the penalties?

Under the Thai Revenue Code, failure to file carries a penalty of 200% of the tax due plus interest at 1.5% per month on unpaid tax. The Revenue Department is increasingly cross-referencing SWIFT data from Thai banks with residency records, and Thailand signed the Common Reporting Standard (CRS) framework which facilitates information sharing with foreign tax authorities. Non-compliance risk is rising.

Does Por.161 affect income earned inside Thailand — for example, Thai rental income or a Thai salary?

No. Thai-sourced income was always taxable under Section 40 of the Revenue Code regardless of Por.161. Por.161 specifically addresses the treatment of foreign-sourced income remitted to Thailand. If you earn a Thai salary or Thai rental income, those tax obligations existed long before 2024 and are unchanged.

Action Steps

- Count your Thai days for the current and prior tax year — determine if you were or are a tax resident under the 180-day rule.

- Audit your overseas accounts — separate pre-2024 savings (Por.162 exempt) from post-2024 income in dedicated accounts, and document the split with dated statements.

- Identify your DTA country and review which of your income types it covers — check rd.go.th for the full DTA text or consult an adviser.

- Obtain a Thai TIN from your local Revenue Department district office if you do not already have one.

- Engage a licensed Thai tax adviser — especially if your annual remittances exceed ฿500,000 or your income includes multiple types (pension, dividends, capital gains).

- File your PND.90 or PND.91 by 31 March (paper) or 8 April (e-filing) for each tax year you are a Thai resident — even if you believe your net liability is zero.